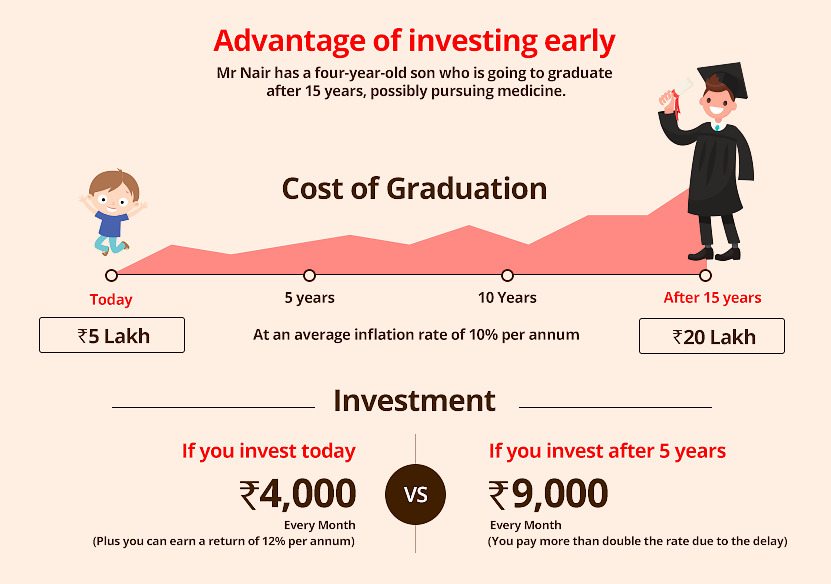

While planning for your child’s needs, the earlier you start the better. If you invest early, it will give you a larger horizon to meet your financial goals such as your child’s education and marriage, and it can even lead to building a bigger aggregation.

Similarly, parents need to have an idea of what corpus value is needed, and when would they need it in the course of their child’s life, depending on their future plans for their child. Select the right investment options so that your portfolio progresses towards each of the financial goals set for your children’s better future.

Here’s how to invest the money:

1. Stocks: It’s important for parents to start teaching their children about managing their finances at an early age, and when it comes to stocks, the goal shouldn’t be any different. Even though the stock market has a reputation of being volatile, equities as an asset—even after adjusting for inflation—will help you meet your financial goals in the long term. So, instead of giving your child his entire pocket money every month, why not keep some back and invest it in shares on his behalf? This will help build a portfolio for him or her over time.

2. Fixed Deposit: Fixed deposits offer investors a higher rate of interest compared to a traditional savings bank account, and opening such an account is quick and easy. For example, you could open a new fixed deposit for your child every birthday. It will be a great way to inculcate the habit of saving. Fixed deposits also assure returns on your investment, making it a safe option to explore.

3. Unit Linked Insurance Plans/Endowment Plans: ULIPs or the investment-cum-insurance plans make an effective low-cost investment option. Some of the ULIPs are even cheaper than mutual funds. The product provides risk cover along with options to invest in any number of qualified investments such as stocks, bonds or mutual funds. As a single integrated plan, both the investment and the protection parts can be managed according to specific needs and choices.

“The child plan we opted for works like an endowment plan, which means, on the maturity of the policy, a fixed amount is returned to the parent. So we paid a premium for a policy that is functional for 15 years and the sum assured is handed over on the maturity of the policy. In a case of death of the parent, our child will get the sum assured, which is the amount the policy has been taken for,” says Ajay Sehajpal, father to a 14-year-old son and 10-year-old daughter.

4. Mutual Funds: Mutual funds have always been a popular investment vehicle for investors because they’re simple to understand and are a great choice for investors with limited knowledge, time or money. It is imperative to maintain your asset allocation by investing in the correct basket of mutual funds. Mutual funds generally buy and sell securities in large volumes, which allow investors to benefit from lower trading costs. One can start with a minimum of Rs.500 in a Systematic Investment Plan (SIP) on a regular basis.

Arun Kumar, who believes that SIP in an equity fund is one of the smarter ways to invest for a child’s long-term needs, says “A SIP of Rs 5,000 started in May 2001 is worth over Rs 25 lakh today.”

5. Life Insurance: A life insurance cover is a critical component of your financial plan because you can name your family members—even children—as beneficiaries in your insurance plan. Doing so sets your children up for a strong financial future and provides for their monetary needs, as and when they arise. Absence of any parent can make things very difficult for the children and the spouse, but by buying a life cover everyone from your spouse to your kids is protected. The insurance can help pay for any immediate expenses, be it medical bills, home loan EMIs or more.

Choose what’s best for you

It is important to bear in mind certain factors while planning: monthly investment amount, maturity dates, consulting a financial expert or consultant for guidance on the plans and policies that are most suitable (taking into consideration the investment amount and the expected corpus to meet the financial goal).Make sure you invest regularly, monitor your investments and insure they help you achieve your financial goals for your children.

Life is not always a bed of roses, but if you’re prepared financially, you won’t have to worry about providing support for your children.

Comments

0 comment