X

Research source

Calculating Your Average Indexed Monthly Earnings (AIME)

List your yearly earnings. Your Social Security benefit is based on your average indexed monthly earnings (AIME). You can calculate this by looking at your annual income each year. Make sure you only include the portion of your income that was subject to Social Security tax. Your covered income includes income from employment for which you were paid an hourly wage or salary, plus self-employment income. The easiest way to get the information you need is to set up an account online with the SSA. From there you can get your Social Security statement and verify your earnings.

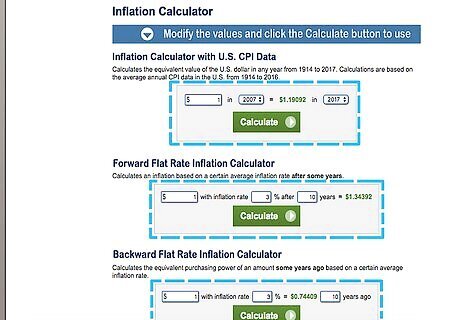

Adjust earnings to account for inflation. If you have earnings decades in the past, the SSA increases these amounts so that all income is expressed in today's dollars. You can make the adjustment yourself using an online inflation calculator. If you're planning on retiring in a future year, you can use an online inflation calculator to estimate the value of the dollar at that time. This is only an estimate and will likely change, but it can still give you a good idea of how much money to expect in Social Security benefits.

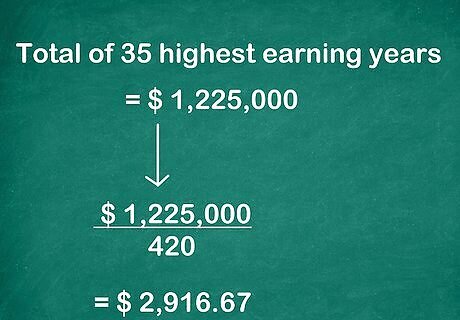

Add up your income for the 35 highest years. Social Security benefits are based on your average earnings for 35 years of work. If you haven't worked for at least 35 years, Social Security will average in zeroes for as many years as you are short. If you've worked more than 35 years, choose the 35 years in which you earned the most income. These are the years the SSA will use to calculate your benefits. If you're currently making more money than you have in the past, and plan on making the same or more money for several years before you retire, add those years instead of past years.

Divide your total by 420. Once you've totaled your 35 highest-earning years, get the average by dividing that total amount by the number of months in 35 years, which is 420. Because you adjusted your earnings for inflation, this average is "indexed." For example, suppose you've made $35,000 a year, adjusted for inflation, for each of your 35 highest-earning years. Your total is $1,225,000. Dividing that total by 420 gives you $2,916.67.

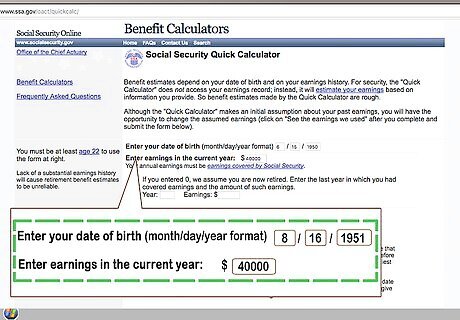

Check your figure with the SSA's quick calculator. Once you've done the calculation yourself and understand how the AIME formula works, you can use the calculator available on the SSA's website to check your results. Go to the SSA's quick calculator at https://www.ssa.gov/oact/quickcalc/ and enter your information. If there's a significant difference between the figure you got and the figure produced by the online calculator, you may want to try to complete the calculation again, or call SSA and find out what caused the discrepancy.

Finding Your Primary Insurance Amount (PIA)

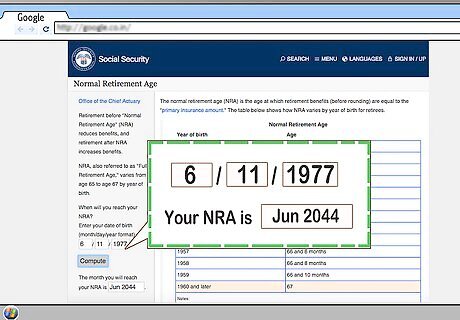

Determine your normal retirement age (NRA). Your NRA, also called "full retirement age," is based on the year you were born, but varies generally from 65 to 67. This is the age at which you will receive your full benefit amount. If you file a claim for Social Security benefits before this age, you'll get less money. Find out your NRA by looking at the table on the SSA website, available at https://www.ssa.gov/oact/ProgData/nra.html. There is also a quick calculator on the side of the page. If you enter your birth date, it will tell you exactly when you will reach full retirement. For example, if you were born on July 11, 1977, you will reach full retirement in July of 2044.

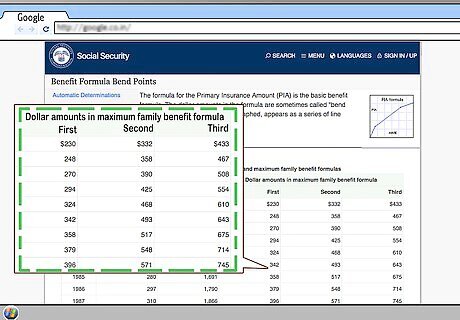

Look up the "bend points" of the formula. When you reach full retirement, you are eligible to receive your primary insurance amount (PIA). This amount is calculated with reference to bend points, 3 separate percentages of portions of your AIME. The bend points you use depend on the year you reach full retirement. Your Social Security benefits are calculated based on these percentages of your AIME. SSA calculates the bend points each year. You can access these numbers through a table on the SSA website. The most recent figures are for 2018.

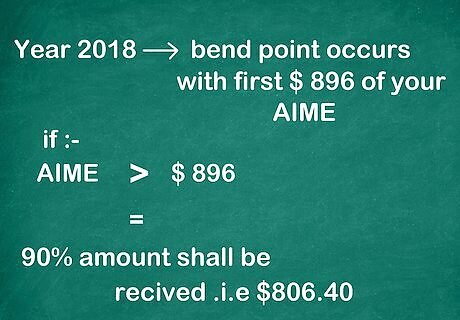

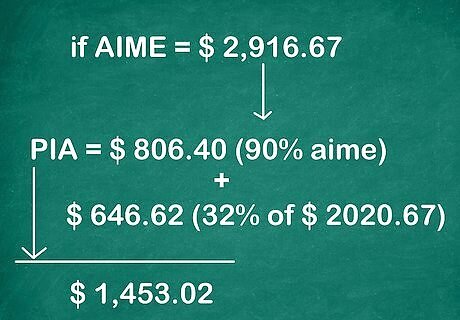

Calculate 90 percent of the first $896 of your AIME. For 2018, the first bend point occurs with the first $896 of your AIME. Provided your AIME is greater than $896, you would get 90 percent of this amount, or $806.40.

Add 32 percent of your AIME over $896 and through $5,399. If you have an AIME greater than $896, your PIA includes 32 percent of your earnings, up to $5,399. If your AIME is less than $5,399, subtract $896 from your AIME and then take 32 percent of the result. For example, if your AIME is $2,916.67, you are entitled to 90 percent of the first $896, which is $806.40. You are then entitled to 32 percent of $2,020.67, which is $646.62. Your PIA would be $1,453.02.

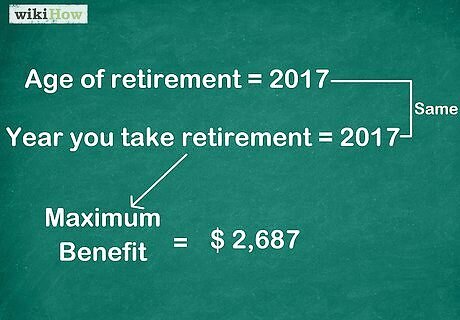

Take 15 percent of your AIME over $5,399. If your AIME is greater than $5,399, you are entitled to an additional 15 percent of any earnings over that amount, subject to the maximum Social Security benefit. The maximum benefit depends on the year you retire, and how old you are when you retire. If you reach full retirement in 2017, your maximum benefit would be $2,687.

Factoring in Credits or Reductions

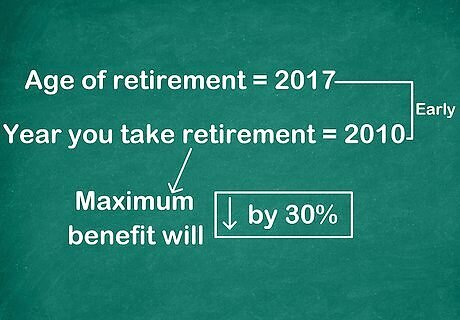

Reduce your benefit if you're retiring early. You can claim Social Security benefits as early as age 62. However, if you claim your benefit before you reach full retirement, your benefits will be reduced by 30 percent. This reduction is permanent, meaning your benefits won't increase when you reach full retirement age. However, if you are disabled or in poor health, it still might be to your benefit to file your claim early.

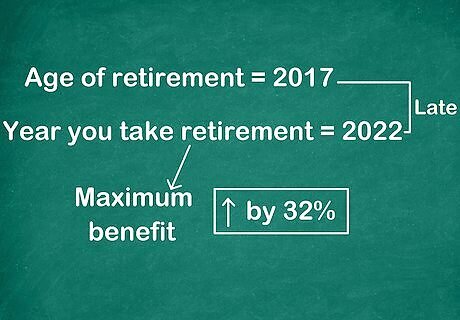

Increase your benefit if you're retiring late. You'll get a credit if you hold off on filing your claim for Social Security benefits past your full retirement age. If you're in good health and plan on working for a few more years, you'll get more money when you do retire. Starting your benefits any time after your full retirement age up to age 70 will permanently increase your benefits by 32 percent. If you plan to keep working, you may be better off delaying your benefit. This is also true if your spouse is still working, since Social Security benefits are also taxable.

Decide whether you plan to keep working. If you don't intend to completely quit working after you file your claim for Social Security benefits, the SSA may withhold some of your benefits. The amount of earnings exempt from this withholding changes every year. For 2018, the exempt amount is $17,040. SSA withholds $1 in benefits for every $2 you earn in excess of this amount. If you make more than $45,360 in 2018 after filing a claim for Social Security benefits, SSA withholds $1 in benefits for every $3 you earn in excess of this higher limit.

Comments

0 comment