Contacting Your Bank

Gather all documentation related to the scam. You will need to prove to your bank or credit card company that you were the victim of a scam. You'll be more believable if you have detailed information about your interactions with the scammers to back up your story. For example, if the scammer contacted you through email, print copies of the emails so you have them for reference. However, do not delete the original emails and rely solely on printed copies. The emails have information in the headers that may be useful for investigators attempting to find the scammers. If the scammer contacted you in other ways, such as through the mail, through text messages, or on social media, make copies of those messages as well. As with emails, save the originals. Compile a chronology of your interactions with the scammers and specific amounts of money transferred. You can use receipts, bank records, or credit card statements for this. Include any information you have about the location of the scammers, even if you doubt its accuracy.

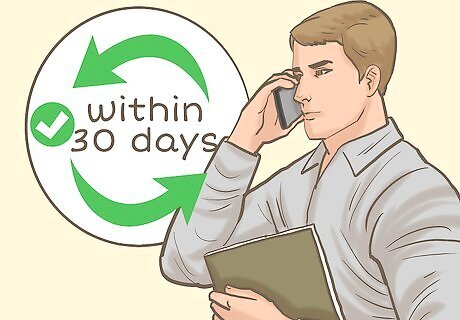

Call the customer service number for your bank or credit card company. Contact your bank or credit card company as soon as possible after you discover that you've been victimized by a scammer. You may be able to recover some or all of your money. However, you generally must notify your bank or credit card company within 30 days of the transaction. Your credit or debit card has a customer service number on the back. Operators typically are available on these lines 24 hours a day. Follow the automated prompts and select the option for reporting fraud. Your bank or credit card company also may have a dedicated fraud line. Check the company's website. For bank transactions, you may also be able to go into a branch during business hours, if you prefer to deal with someone face-to-face.

Provide information about the scam to your bank or credit card company. Remain calm, and describe the facts of the scam in chronological order. Be as detailed as possible, including the date and amount of the transaction. If there were multiple transactions, be prepared to explain why you sent the scammers more money. Take the name and any identification number of the customer service representative you talk to. Ask if they have a direct number so you can talk to them again if necessary. If you have physical documentation, find out how you can submit it. Request written confirmation of the conversation be mailed to you. When you get it, save it with your own notes. Doug Shadel Doug Shadel, Fraud Expert & Bestselling Author If you realize you've fallen victim to a scam and money has already exchanged hands, act swiftly in contacting relevant institutions. Notify your bank and credit card companies, file complaints with the FTC, and document all details of the scam. Though recovery is difficult, being proactive gives you the best chance of getting funds returned.

Answer follow-up questions from your bank or credit card company. Your bank or credit card company likely will initiate an investigation of the scam. The money may be provisionally credited to your account. However, you'll need to stay in touch to make sure you get your money back. For example, your bank or credit card company may want a copy of the police report. Send it as soon as possible. You may also be able to take it to a local branch in person. Keep a record of all communication you have with your bank or credit card company, including the dates and times of any phone calls and the name of the person you spoke with.

Follow up if you don't hear back within 30 days. US law requires your bank or credit card company to at least acknowledge your complaint and initiate an investigation within 30 days of your call. Many other countries, such as Canada and the UK, have similar laws. If a month passes and you hear nothing, call the customer service number and ask about the status of your complaint. Banks and credit card companies are expected to resolve the matter within 2 billing cycles, which normally equates to 2 months. In any event, they cannot take longer than 90 days under consumer protection laws. Keep in mind that resolving a complaint does not necessarily mean that they find in your favor or refund your money. If the bank or credit card company rules against you, you might want to talk to a consumer protection attorney to explore further options.

File a complaint with a government agency if your claim is refused. If you present reasonable evidence that you were the victim of a scam, your bank or credit card company may be legally obligated to refund the money. Government agencies that protect consumer rights can help you get your money back if your bank or credit card company refuses to cooperate. For example, in the US, you can file a complaint against your bank with the Consumer Finance Protection Bureau (CFPB) by going to https://www.consumerfinance.gov/complaint/. Once you file the complaint, your bank or credit card company has a limited time to respond. Most complaints are resolved within 2 weeks. You may want to talk to an attorney about getting your money back from your bank or credit card company. Most consumer attorneys provide a free initial consultation, and you can discuss your options.

Working with Law Enforcement

Call your local police department. All police departments have non-emergency phone numbers that you can call at any time if you want to report a crime. Some larger departments may have specific numbers dedicated to reporting financial crimes, including scams. In the US, you can find contact information for local law enforcement by visiting https://www.usa.gov/local-governments and selecting your state from the drop-down menu. Do not use emergency numbers, such as 911, to report a scam, unless you feel your life is immediately in danger.

Collect documentation related to the scam. Local police will be more likely to investigate the scam if you have specific documentation of your interactions with the scammers. If local police are able to identify the scammers, you may be entitled to restitution through criminal courts. Include as many details as possible that could help investigators locate the scammers. If the scam occurred online, keep original digital copies of emails or messages in addition to any screen captures or printed files.

Submit a report to local law enforcement. When you talk to an officer, be as clear and detailed as possible. Stick to the facts, and avoid introducing any speculation about the identity or motives of the scammers if you don't have any direct evidence. Get the name and badge number of the officer who takes your report. The officer will also give you a report number. You'll need it to get a copy of the written report when it's ready.

Pick up the official written report. The officer who takes your report will let you know when the written report will be ready. You'll likely have to make another trip to the precinct to pick up a copy of the report. Make copies of your written report when you get it. You may need to submit it to your bank or credit card company, or to other government agencies.

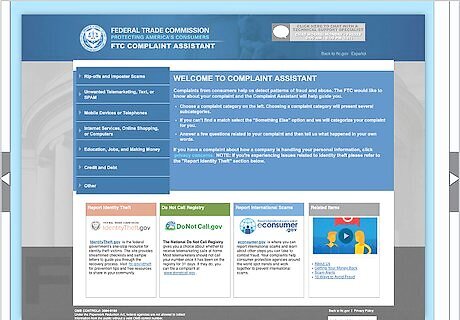

Report the scam to consumer protection agencies. Government agencies compile reports about scammers for faster attempts to get money back from scammers. Different federal, state, and local agencies may get involved, depending on the type of scam. For example, in the US, the Federal Trade Commission (FTC) investigates and builds cases against scammers. You may be able to recover some of your money from an FTC lawsuit or settlement. The FTC has a complaint tool on its website that you can use to submit a complaint. US state attorneys general have anti-fraud departments that also investigate and prosecute scammers. Go to the website of your state attorney general to learn how to submit a complaint or report.

Cooperate with any continuing investigation. Because of the difficulty of tracking down scammers, police may not do more than a cursory investigation. However, if they do manage to identify the scammers, you may be called upon to talk to prosecutors or testify at trial. If the scammers are caught and brought up on charges, you may be able to get some or all of your money back through criminal restitution. You'll only be able to get back the money you can prove you paid to the scammers, so make sure you keep all receipts, bank or credit card statements, and other documentation.

Avoiding Future Scams

Educate yourself about common scams. Many government agencies and consumer protection organizations have lists of common scams on their websites. If you learn to recognize a potential scam, you can protect yourself from falling for another one. There is a massive list of many different types of scams available at https://www.usa.gov/common-scams-frauds. This list not only describes common scams but also tells you what to do to keep from falling for them. Generally, be skeptical about any communication you get from someone you don't know. Take steps to verify that they are who they say they are and don't give them any personal or financial information. If you receive an email or letter in the mail telling you that you've won a contest or sweepstakes that you never entered, be wary. Remember the adage that if something seems too good to be true, it probably is.

Assess the security of your personal and financial information. Change your passwords and sign up for enhanced security features, particularly if the scammers gained access to your personal information. You may want to get new credit or debit cards issued, or change your account numbers. If the scammer contacted you through email, you might consider changing your email address. Once a scammer identifies your email as a target, they may share this information with other scammers. If the scammer contacted you through social media, tighten your security settings so you can't be contacted by people you don't know. Avoid discussing the scam online in public forums or mentioning how much money you lost. Other scammers could read these posts and use the information to figure out how to target you again.

Stop communicating with scammers immediately. The scammers may contact you again and offer you an "opportunity" to get some or all of your money back by doing something for them. This is a follow-up scam, an attempt to get more money out of you. Change the settings on your email account so that emails from the scammers are immediately deleted or sent to spam. You also may be able to block the email addresses the scammers used. However, they may use different email addresses. You can also set up filters to send emails to spam if they contain certain keywords.

Delete suspicious emails or texts. One common follow-up scam involves the scammer posing as a member of law enforcement, or employee of a nonprofit or government agency. These emails offer to investigate your situation and recover your money for a fee. However, you will never be charged a fee by a legitimate agency to investigate a scam or fraud claim. Scammers also may pass on your information to other scammers. Follow-up scams may happen immediately after the original scam, or months later. A follow-up scam may seem completely unrelated to the original scam. The scammers may attempt to manipulate your emotions or play on your fears. If you get an email or text from out of the blue and you don't recognize the sender, assume it is a scam and delete it immediately. Generally, don't respond to any email or text that comes from someone you don't know, or from an address or phone number you don't recognize.

Add your phone number to the "Do Not Call" registry. You can get your number on the registry by calling 1-888-382-1222. Having your number on the registry may not eliminate all scam calls, but it will keep a lot of scammers from getting your number. As with email, if the scammer initially contacted you by telephone, you might want to consider changing your number. On a mobile phone, add individuals and businesses that frequently call you to your contacts. If you receive a call from a number that you don't recognize or that isn't listed in your contacts, don't answer the phone.

Contact government agencies directly to verify unsolicited emails. Government and law enforcement agencies typically won't send you unsolicited emails or texts. If you get a message from someone claiming to be a law enforcement or government officer, call the agency they claim to represent and report the communication. Some hallmarks of a scammer impersonating a government official include typos or misspellings, as well as grammar and punctuation errors. Scammers also use alternate characters to make their email addresses look like an official government address. For example, they might use a lower-case "l" in place of a capital "i," since the two letters look the same in most email fonts. To check this, copy the email address and paste it into a word document, then change the font. If a scammer attempts to impersonate a law enforcement officer or government official, save the email or text to share with the agency. It may include information they can use to track down the scammers.

Comments

0 comment